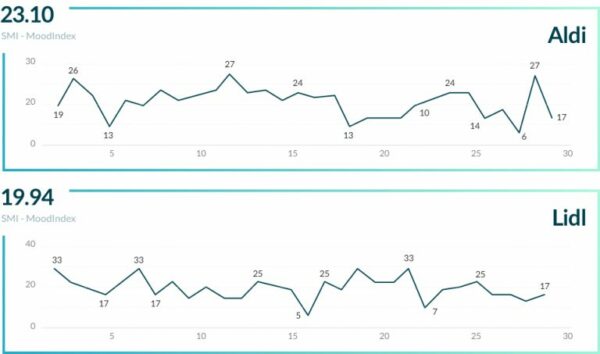

The analysis showed that the SMI rating gave interesting hints to follow down to a more granular level. What we saw were two German grocery discounters which settled into the competitive US market. Both are greatly appreciated by the consumers for their crisis handling skills and staff, but both also shine for their own specific reasons. While Aldi’s positive reputation is driven by the appearance of their stores and employees, it’s the price which is driving sentiment up as well.

The analysis showed that the SMI rating gave interesting hints to follow down to a more granular level. What we saw were two German grocery discounters which settled into the competitive US market. Both are greatly appreciated by the consumers for their crisis handling skills and staff, but both also shine for their own specific reasons. While Aldi’s positive reputation is driven by the appearance of their stores and employees, it’s the price which is driving sentiment up as well.

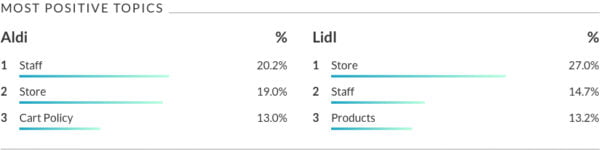

For Lidl, it is the product portfolio that excites their consumers. Not to forget, Lidl appears to be a brand with a significantly higher margin of rational consumers, who till now have not been wholly satisfied. In contrast, Aldi is a brand mostly driven by the very positive perception of their slightly larger emotional consumer segment. They also appear to do a better job with their rational consumer segment, even if it displays a smaller margin of consumers to them.

All in all, it can be said that both brands are doing a great job in times like these. It also turns out that brands which are not famous for having the largest online communities appear to have vital open discussions taking place on their social media profiles. We could even apply additional AI modules to extract insights on gender and age, but even with these comparably low efforts, the brands’ personalities begin to take shape.

If you’re interested in an investigation on your specific use case or any of our AI capabilities, feel free to reach out to us. We’ll be more than happy to walk you through our understanding of text analytics and the latest use cases of artificial intelligence.

Stay tuned for our upcoming comparisons.